Whether you are remarrying after a divorce or the death of a spouse, it is important to enter your new marriage with smart financial planning. There are many things to consider, including how you will handle your current financial needs and future financial wishes.

Assets and Liabilities

First, conduct a thorough review of both of your assets and liabilities. Your assets include bank accounts, stocks, bonds, house, car, retirement plans, insurance contracts and other investments. Liabilities may include credit card balances, student loan debt, car loans, mortgages, etc. Be aware of the rules in community property states (Arizona, California, Idaho, Louisiana, Nevada, New Mexico, Texas, Washington and Wisconsin), where asset ownership is much different. In these states, the law presumes assets will be owned jointly.

Day-to-Day Financial Management

Next, consider how you will manage your financial obligations on a day-to-day basis. How will your monthly bills get paid? Some couples combine their checking accounts, while others continue to maintain separate checking accounts and create a new joint account into which both parties contribute each month. Joint expenses are paid fromm the new account and certain personal expenses continue to be paid with individual accounts. (For related reading, see: Should You Open a Joint Bank Account?)

Who will be responsible for getting the income taxes prepared every year? Who will pay the income tax liability? Is it better to file jointly or married filing separately? Who will manage the investment accounts? How will all of the financial responsibilities get split up? These details should be discussed.

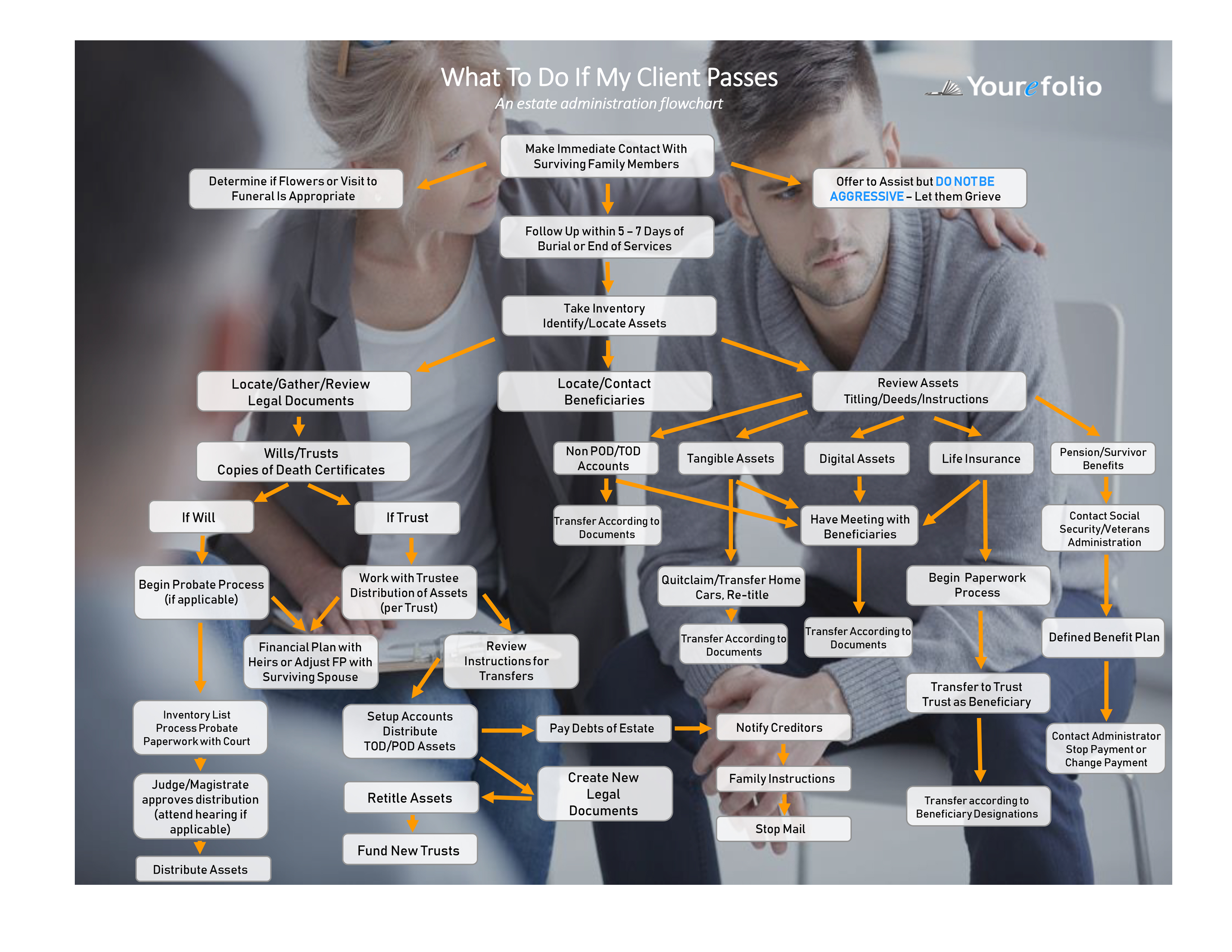

Check Your Beneficiary Designations

Retirement plans (such as IRAs, 401(k)s, etc.) have named beneficiaries that should be reviewed and potentially updated.

In addition, insurance policies and annuities have named beneficiaries. Getting married is the perfect time to review who is currently named and decide who you wish to be named. Any agreements made during your first marriage could potentially inhibit your ability to update your beneficiaries and should be reviewed as well.

Estate Planning Updates

A will, also known as a last will and testament, is a document that states your final wishes. It outlines how certain property gets distributed to your heirs. It is also where you name guardians for minor children and your executor, who will make sure your wishes get carried out.

A second marriage is a good time to review your will to determine if you should execute a new one or make changes to the existing one. Blended family dynamics can also come into play when reviewing your estate plan. If either spouse has children from a previous relationship, adjustments to your plan may be necessary. (For related reading, see: Estate Planning Basics.)

Trusts and Trustees

A variety of trusts, such as a bypass trust, qualified terminable interest property (QTIP) trust or spendthrift trust can provide useful ways to transfer wealth to children while imposing some constraints.

Dividing your assets between a surviving second spouse, children from that marriage and children from your first marriage(s) can potentially cause friction. A helpful solution to this problem is to give an independent trustee the ability to make adjustments so everyone is treated fairly and according to your wishes.

Health Care Proxy

A health care proxy allows you to delegate your health decisions to another in the event you cannot make them yourself. If you previously designated your first spouse, you may want to update this.

Power of Attorney

Your power of attorney is also something to carefully consider. This legal document establishes the right for another person to act on your behalf regarding financial assets, including the potential for making gifts and changing beneficiaries. It’s common to give this power to a family member, however in a blended family that could cause conflicts. Again, appointing an independent party from outside the family could be beneficial, giving them durable rather than general power of attorney.

With thoughtful planning, you can meet your family’s fiscal needs and create a strong financial future with your new spouse.

View original article here