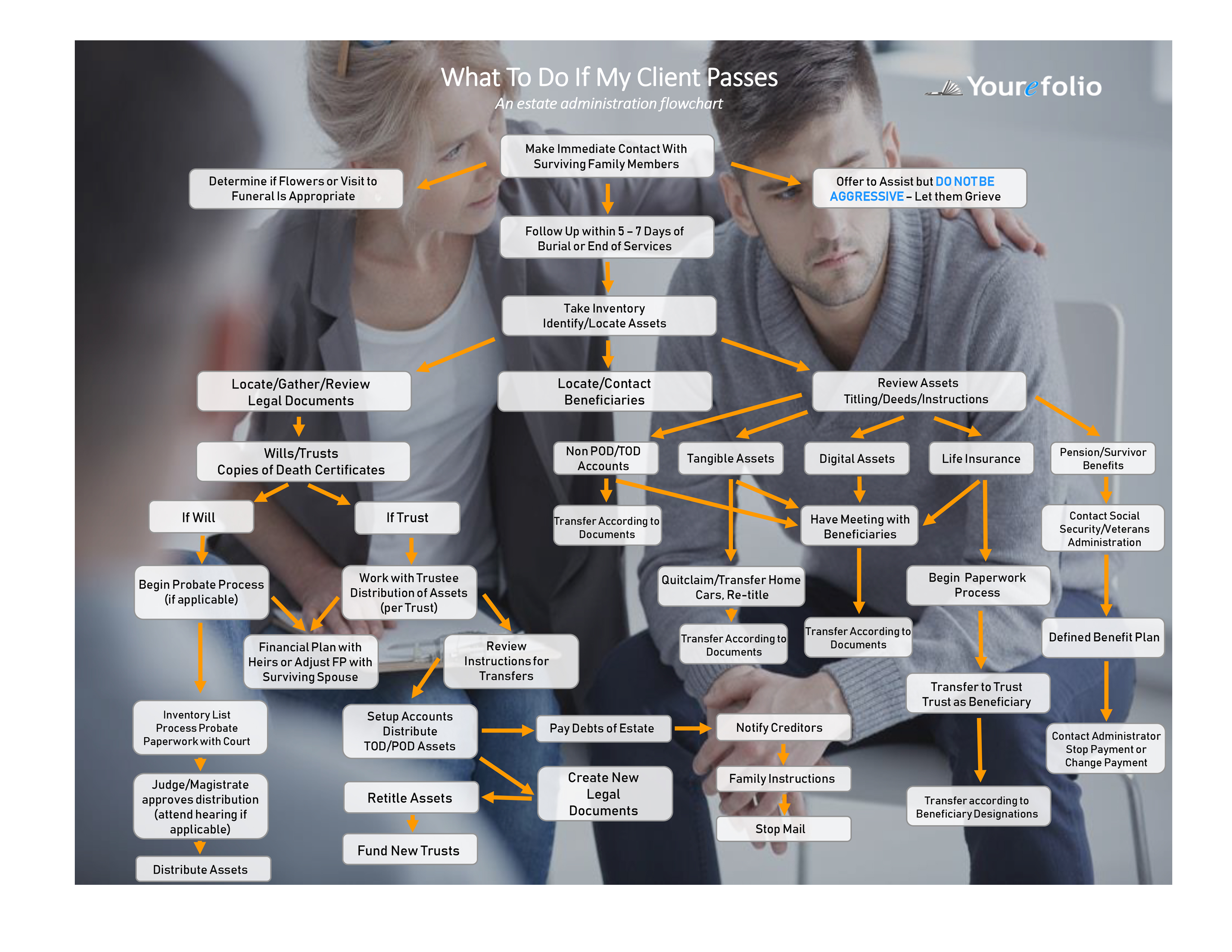

Estate planning for retirement assets like IRA’s and 401(k)’s, which make up a third of investments for middle/upper-middle class households, can be the largest asset outside the equity in a family’s home. Estate planning for these tax-deferred assets can be challenging and therefore should be planned for carefully. Below are some basic items to make sure families can make the most of their inherited retirement assets and make sure they transfer with ease.

Make sure all planners account for financial planning when estate planning

It is critical for financial planners and investment advisors to work closely with estate planning attorneys because careful collaboration can alleviate issues. One person may see something another has not. Multiple eyes on an estate plan can be more effective. Often, clients are whisked off to an estate planning attorney and there is little collaboration between the financial and estate planning. It is imperative when including income needs into the estate plan that all assets, including tangible ones, are taken into consideration. The way they are distributed upon death may need to have pertinent reflective language in the corresponding estate planning documents.

Make sure beneficiary information is correct

Retirement assets are transferred to designated beneficiaries named on each retirement account. Not accurately reflecting beneficiaries is one of the biggest mistakes that can be made. Not having a beneficiary and/or not making sure beneficiary designations reflect the current situation can cause delays and headaches in the transfer. Delays and issues with the transfers can reflect equally on cash flow needs of beneficiaries. As part of reviews, check with the clients on their wishes, current income needs and designations.

Lack of planning for contingent beneficiaries in retirement assets

Even when clients have successfully created beneficiary designations, issues can still arise. Making sure that contingent beneficiaries are accurately reflected or updated accordingly is equally important. Typically, little thought is given to reviewing continent beneficiaries. However, there are many instances when contingent beneficiaries inherit assets, especially contingent beneficiaries who are younger than the primary beneficiaries. Financial advisors and estate attorneys can help their clients by reviewing contingent beneficiaries carefully to steer off any future issues.

Capitalize on the stretch provisions

Younger beneficiaries can stretch mandatory withdrawals preserving tax deferral and increase the value of the account. Choosing an older beneficiary can potentially reduce the stretch exposing heirs to higher taxes. This may cause assets to be withdrawn in amounts not planned for. Spouses have even more options to stretch the distribution requirement. Periodically review this provision to make sure it fits with your clients’ current needs.

Use of Trusts as a beneficiary of a retirement asset

Often little thought is given to how trusts can play into retirement asset beneficiary designations. First, they can provide protection for the beneficiaries themselves. If you have a beneficiary who cannot control their spending or has special needs, often a trust as the beneficiaries can help. When using a professional to administer an estate, the effective use of a trust as a beneficiary should be discussed. Considering the use of a trust for a retirement asset should be carefully approached as it may cause other issues. Always consult an expert when considering a trust as a beneficiary.

Retirement assets are one the largest in this trillion-dollar wealth transfer occurring currently. Advisors who plan to capitalize on this wealth transfer or minimize losses from beneficiaries moving assets away need to plan with their current clients. Focusing on retirement assets is a good start considering the impact they have on most of an advisors’ client base. Always consult with other professionals as to the most effective way to plan for retirement assets in your client’s estate plan.