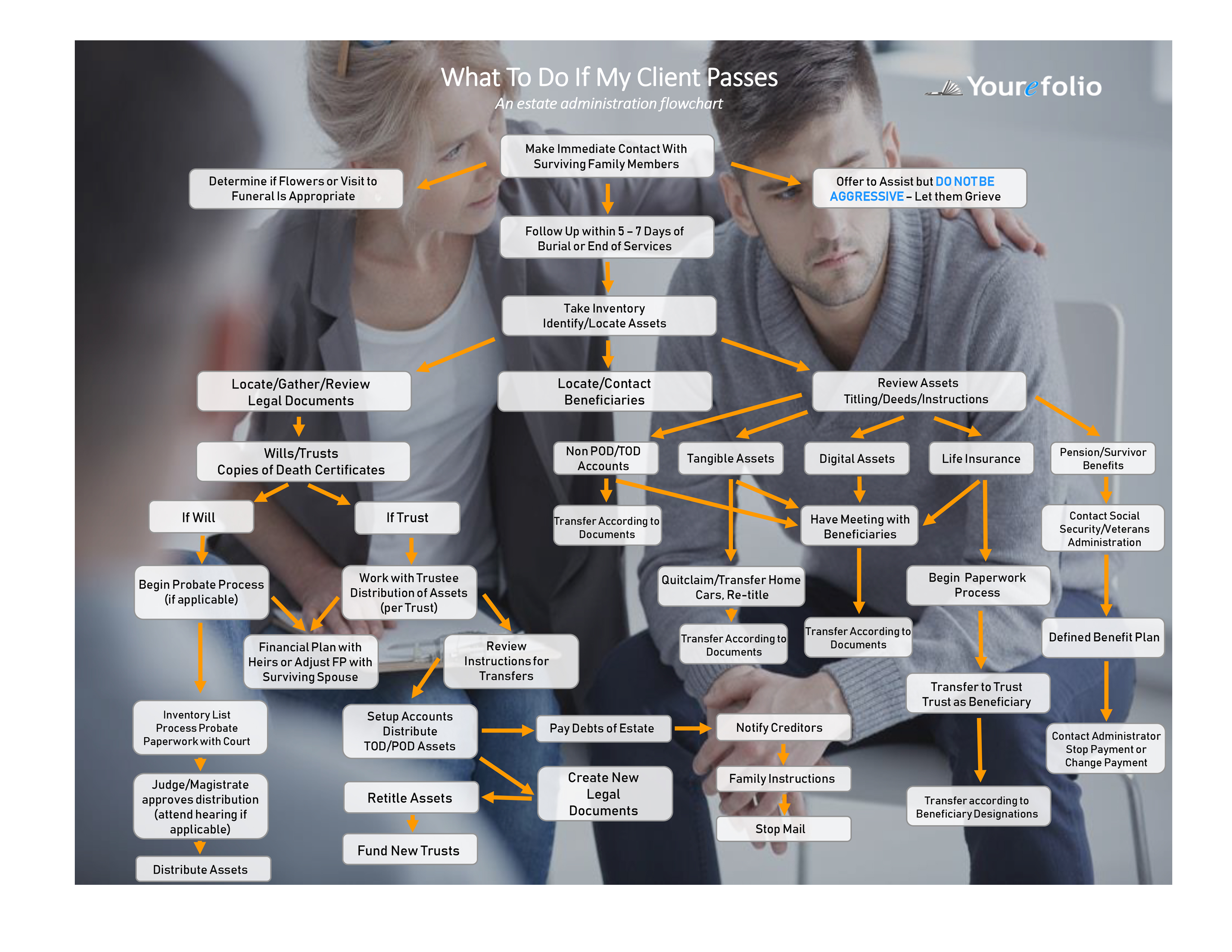

The Yourefolio Staff

Let’s face it, when it comes to estate planning, the focus always seems to be directed at reducing tax implications. The reality of estate plans is that taxes affect less than .2% of the population1. While there are many opportunities to reduce taxes within someone’s estate, the reality is that estate planning provides for so much more than just a reduction in taxes.

The challenge is crossing the line between legal advice and planning. For this reason, most advisors simply connect their clients to an estate planning attorney. This is where the severe disconnect comes in because the truth is, it’s the advisors’ relationship. By disconnecting yourself from the process, can you be certain that your client gets the best estate plan for their situation? The estate planning attorney will have questions that you can answer, but will you be asked? Other than legal expertise, the attorney may not understand or be able to communicate all aspects of your client’s lives because they simply have not been involved for a period of time and may not know your clients or their beneficiaries as well as you do.

Understanding all the benefits estate planning has to offer and how to facilitate them can seem overwhelming. The reality of the planning part is simply that, the planning. It is not giving legal advice, it’s laying the groundwork to illustrate a client’s current path, items they may need to address and then a plan of attack to reach their goals. Other than the actual documents being drawn up, an advisor can facilitate the entire process including; funding, review and somewhere down the road, settlement. Why aren’t more advisors facilitating the estate planning process, and getting an attorney involved at the end, when documents need to be drawn up? Is it that advisors don’t get paid for estate planning? Is it that the attorney charges so much that advisors don’t want to increase the bill by doing all the upfront planning? Is it a lack of expertise and thus the advisor does not feel comfortable leading the planning process? Could it be that the advisor knows that at the end of the day, documents must be prepared, so why get involved anyway? Whatever the reason, estate planning is essential in the practice. All it may take is a quick refresher of how to analyze an estate plan, prepare the items that need to be addressed and ultimately, facilitate a plan that can be delivered to an estate planning attorney to the have documents prepared.

It Begins by Obtaining Pertinent Information

Unfortunately, over 60 percent of Americans do not have an estate plan or even a will. What an opportunity this creates for advisors! The challenge is, facilitating the conversation. Its starts with understanding. Most clients are focused on taxes and asset transfer. They truly don’t understand the value of estate planning and all the benefits it can provide. Advisors must ask the right questions to move beyond the assets. Questions such as, do you know how you want your legacy to live on, are your assets protected from creditors, how do you intend to protect assets from government seizure should you need long term care and other questions centered around the benefits of estate planning?

Obtaining the right information is not limited to an asset inventory list alone. While an asset list is important, open ended goals and concerns are the foundation of beginning any estate plan. Ask questions that make your clients think outside the box. Generating open ended thoughts can uncover opportunities to help you and your clients create a proper estate and legacy plan.

Prior to creating your questions, understand what estate planning can do for your clients. Are your clients young? Do they need guardianships or life insurance planning? Do they need to establish protections for their business or from potential creditors? Do they want to control distributions to take care of family members? Make a list of all the benefits of estate and legacy planning and then ask questions centered on them.

Another important aspect in the initial planning is understanding how pass on hard to divide assets. These often cause issues amongst beneficiaries. It is easy to distribute a bank account, but a vase on the mantle which has been in the family for 30 years is extremely difficult to split up. Sometimes hard to divide assets need attention before they can be liquidated or transferred. The point is that, very little attention is given too hard to divide assets.

Present odd scenarios that happen in our everyday lives, to ensure all I’s are dotted and all T’s are crossed. Consider ex-spouses of children, multiple generations, aunts and uncles who may need money. People act differently when they realize or believe they are entitled to an inheritance. Beneficiary designations and wills can be challenged, so make sure no stone is left unturned which could open the door to a beneficiary challenge.

Present Applicable Solutions and Develop a Plan

Presenting applicable solutions is not providing legal jargon to solve an issue. This is real life and real people. Applicable solutions are derived from understanding what your clients would like to transpire in the end. The legal language formulated in a document is ancillary to the actual solution. For example, if they have hard to divide assets, who and how would they like them to be handled? Is there a more responsible adult who can handle it? Does there need to be money set aside for repairs? Answers to these questions are the applicable solutions to which language in documents will support.

Most clients will have some type of retirement asset. This could be a defined benefit pension, a ROTH IRA or Traditional IRA. Understanding how the surviving spouse or beneficiaries can utilize distributions goes a long way in the planning process. Advisors will have a better understanding of the financial flow to the surviving spouse or beneficiaries, which is an important part of retaining assets and estate planning.

Remain in the Process

At a certain point your clients will have to agree on a plan for all the items you address. At this point, there is no way around engaging an attorney to have legal documents drawn up. Please do not use document prep software to prepare the documents. This is just a disaster waiting to happen. Choose a competent attorney through research or ask colleagues for referrals. Remember, these are your clients so your recommendation is vital to the plan success.

When the documents have been drawn up, work with the attorney to develop an understanding of what they have done to support your clients plan. Ask for recommendations they may have for solutions if there was something you overlooked or couldn’t develop on your own. Staying in the process is the key for success for you and your clients.

Estate planning can be done by any advisor and provides so many benefits to your clients beyond facilitation of the transfer of their assets. Don’t assume that your client needs $11 million dollars to engage in estate planning. Any client, in any demographic can benefit from estate planning. Remember, it all starts with a conversation and understanding. This is the hardest part of the planning process. The rest is just the icing on the cake.

1 Money Magazine - Alicia Adamczyk August 9, 2016 2 AARP - Barbranda Lumpkins