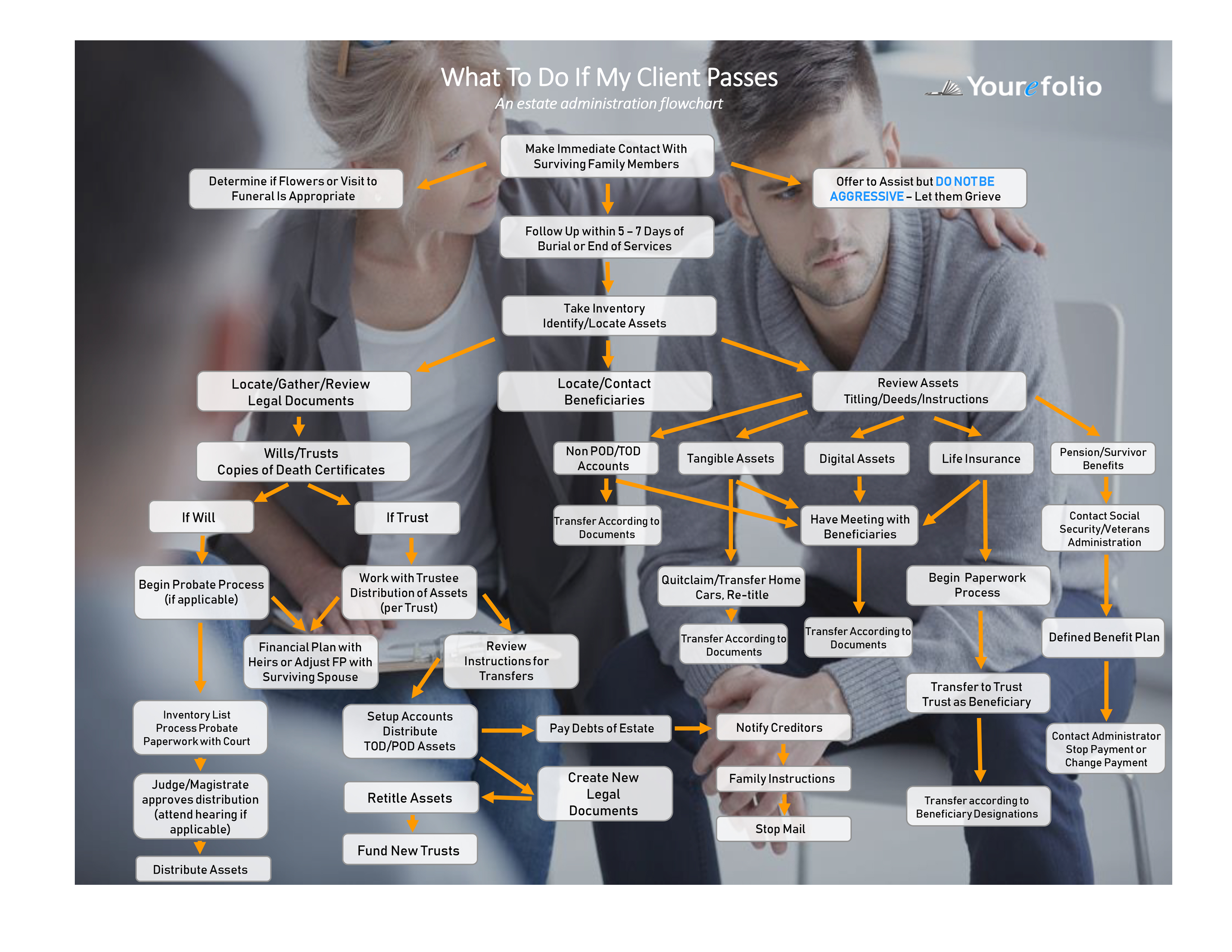

Five Simple Estate Planning Items That Could Cause Issues for Your Clients

We know you are on top of their financial lives but it can be challenging to stay focused on their estate planning. Since it is an area of planning that requires the involvement of an attorney, it is a topic most advisors don’t really address or get involved in the details. Here are some simple concepts that you can assist with that will help your clients’ estate plans today.

1. Procrastination or not moving your client forward in the process

There is no incentive to plan for death. Who even wants to think about it? Most clients don’t believe anything will happen to them until they get older. The problem is we really never know when it is our time. Now you can move your client’s process forward, even if you need to engage an attorney. Explain the value of having an estate plan in place and the benefits like guardianship, protection of assets and health care directions in case they are incapacitated. Even a basic will helps if they unexpectedly leave. There are many ways to start the conversation but there is no better time than the present to get your client’s estate plan in motion.

2. They Have Never Updated Their Plans

Maybe they were proactive and started planning for their estate long before your relationship, but do you know if they have ever updated those plans? The only constant in life is change, and our estate plans must account for that. If your clients have moved to a different state, your plans should adhere to the laws in your state of residence. Have they divorced, remarried, or had more children? Have any of your beneficiaries or executors died since you drafted the plans? Have relationships changed or the health of beneficiaries? Their estate plans should reflect their estate as it is currently, not as it was. Estate plans should be consistently updated as clients’ lives change.

3. A Trustee Was Named But Never Consulted or Their Ability Known

It is common to assign trustees based on personal feelings, but this is a major mistake in estate planning. Clients name close friends or relatives as trustees but never consult with them or even know if they have the capabilities to handle (and are willing to handle) all of the responsibilities entailed. They certainly don't want to burden someone who is incapable or unwilling with the administration of your trust. Have the discussion to consider appointing a neutral third party as trustee--a bank or an attorney--to avoid any such issues if they don’t have a competent person for trustee. Make it part of the conversation.

4. The Plan Only Addresses Liquid Assets, Not Tangible Ones

The estate plan assigns responsible trustees and ensures beneficiaries are current on the life insurance policies and retirement accounts. The current plan also reflects the client’s current circumstances so the estate plan is full-proof, right? Not Quite. Sometimes the focus is on the big picture, that plans forget the little things, and those little things can be cause the biggest issues. Kids fight over money, but they also fight over heirlooms, mementos and other tangible assets. Adult siblings have broken relationships and stopped speaking over things like who receives their mother's favorite costume jewelry or their father's beloved sports memorabilia. Their heirs will want to remember them by more than just the checking account or their money.

5. Digital assets are not accounted for in the Estate Plan.

Technology may have changed most Americans’ day-to-day lives, but it’s also having an impact on how it should be addressed in death

Many people are living most of their lives online so the idea of what an assets is needs to be expanded. The assets doesn’t only have to have monetary value, it can have sentimental value. Digital assets include, for example, photographs on a hard drive, downloaded music from an online streaming service, and bitcoin, which only exists online. Digital accounts cover everything from email, PayPal and Facebook, to accounts with financial institutions, eBay and Amazon,

If the estate plan doesn’t outline the digital assets or that they even exist, it’s going to make it difficult to manage the person’s affairs when they pass. There may also be assets of which the attorney or the executor is unaware. Understanding that sharing passwords does not entitle someone to the digital asset. It is imperative that estate plans are updated to reflect a client’s digital assets.

There is never a bad time to entertain the conversation about estate planning. Some of these tips above will help facilitate a conversation. Just letting your clients know you are on top of their financial lives but their next generation of wealth can go a long way.