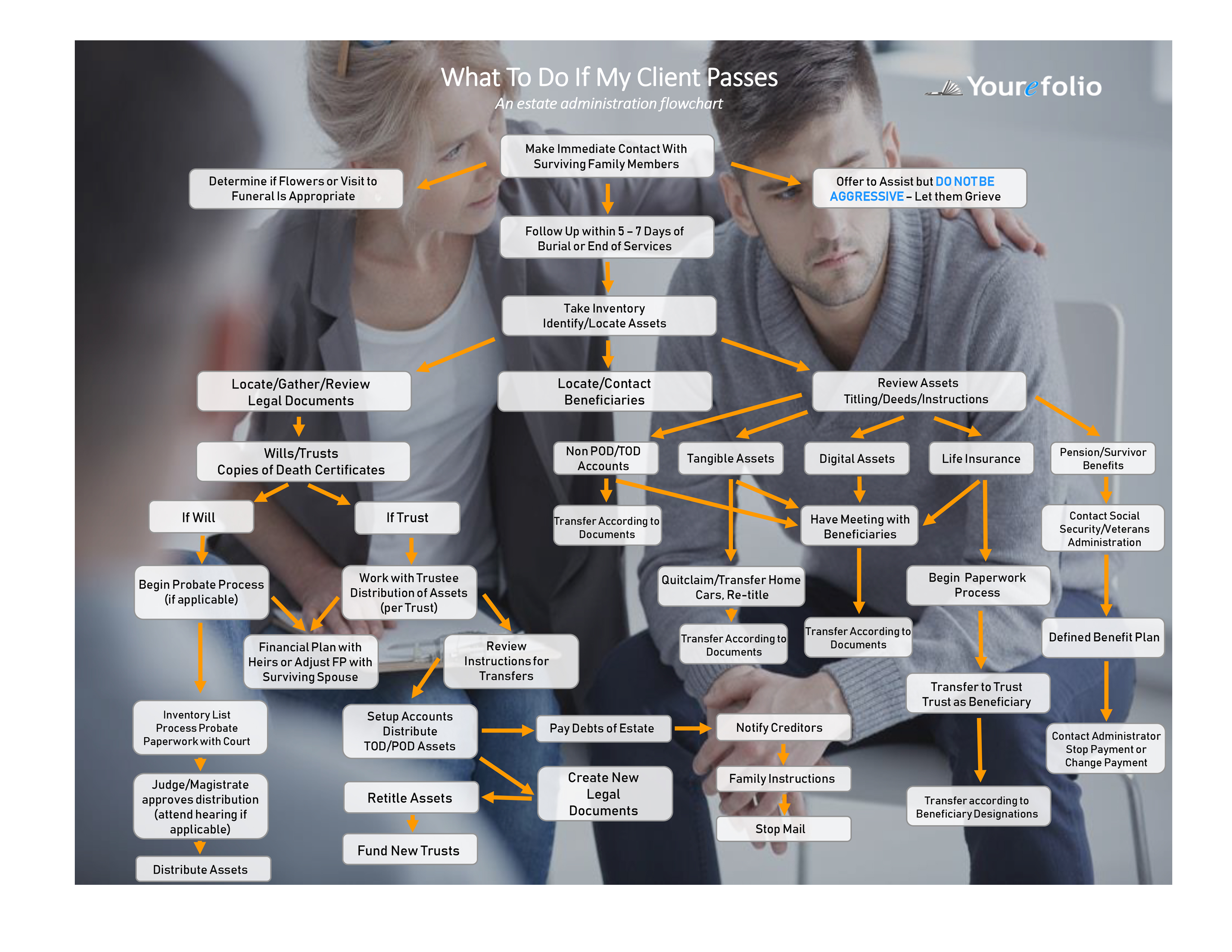

It is no secret by now that the Secure Act, “Setting Every Community Up for Retirement Enhancement (SECURE) Act,” implemented in January of this year, threw a twist in how planners work with the next generation of wealth.

Prior to January 2020, planners could use the Stretch IRA to spread payments over the lifetimes of beneficiaries. That is all but gone now, so a little creativity is needed to help beneficiaries plan for the longevity of those assets. The good news is it created a planning opportunity for advisors and attorneys. The bad news is it made some trust provisions irrelevant.

There are a few creative strategies that remain to help out certain beneficiaries affected by the law but before the options are considered, it is important to know where that beneficiary fits in.

Spouses, minor children, disabled beneficiaries, or those with chronic illness and those that are not more than 10 years younger than the decedent are exempt from the 10-year withdrawal period. Non-designated beneficiaries such as entities and charities are also exempt from the Act.

All other beneficiaries have new rules; therefore, some careful planning and a little creativity can help those beneficiaries who need to stretch payments out over their lifetime. There are many things to consider so a comprehensive plan is best. As you plan with for the changes with this Act, here are some options to consider and plan with those future generations.

Roth IRA conversions are now a type of account that needs to be considered. Of course, the advantage is all future withdrawals are tax-free. Beneficiaries can stretch these accounts for as long as they would like with the tax-free withdrawal advantage. The challenge is paying the taxes as part of the conversion. Depending on the IRA account holder, this could be an option for future generations and stretching out the inherited IRA.

Life insurance is another option to cover taxes and income needs. Withdrawals can pay premiums for certain type of life insurance vehicles. Then, upon the passing of the account holder, beneficiaries will receive the proceeds of the life insurance tax free as the inheritance. The challenge is that permanent life insurance policies can be expensive, the account holder may not be able to be written for insurance, and growth of the account can be limited.

Charitable trust planning can provide an option for stretching out the inherited IRA. Charitable trusts are irrevocable trusts that have their own separate challenges. However, these types of trusts typically pay a benefit and when the beneficiary passes, the remaining amount goes to a charity. Managing these types of trust have their own challenges but for overfunded IRA’s and high net worth clients, this can be a consideration.

Account holders can always move withdrawals or portions of withdrawals to taxable accounts. While this is not ideal, it does allow for a step-up provision upon inheriting and savings on potential capital gains taxes.

The challenge with the new 10-year withdrawal rule is distributions are taxed at ordinary income and the types of beneficiaries affected are in their highest earning years. This causes more of a tax liability because typically they are in higher tax brackets. While there are no rules on how it has to be withdrawn (ie; every year, every month), whatever balance remains at the end of the 10-year period will be taxed. Proper planning now can make all the difference. Planners now should take advantage of this opportunity to review the estate plan and make adjustments for this new Act.